Addressing What it Takes to Win with the Audience

Right after the Emmys, we were analyzing all of the bits and pieces trying to figure out who the kingpins in the industry were going to be when we read a statement with so much bravado that we blew coffee out of our nose … gawd, that burns!

Marking what seems to be the end of the good old broadcast TV era, HBO had taken home statues for Game of Thrones, Chernobyl and others while Netflix and Amazon received a decent number of trips to the stage.

But most of the ads during the evening were for the new breed of TV shows; spots for Apple TV+, Netflix, Hulu, Amazon Prime, Hulu and Disney +.

So why the coffee/nose bit?

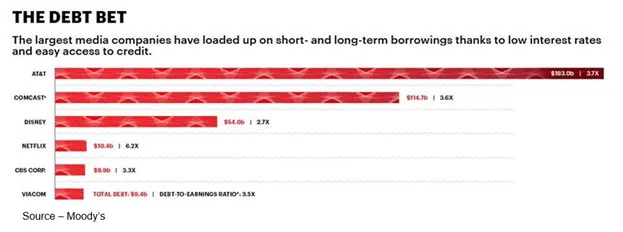

Richard Greenfled, media analyst at LightShed Partners, noted that of all of the potential streaming services, AT&T-owned WarnerMedia was in a unique situation because:

- HBO has an estimated 38 M US subscribers

- Has Friends, Game of Thrones, Big Bang Theory

- An extensive library of content

According to him, because of this, a “significant number” of subscribers will be willing to pay “a few bucks more to get a whole lot more content.”

Hate to crush his grapes, but we’ve never watched Friends or Big Bang Theory, have no idea if we’ll like what’s in their “extensive library” and doubt if we’d pony up “a few bucks more!”

In addition, IMO, the family has enough subscriptions (Amazon Prime, Netflix, Apple TV+, preordered Disney + and CBS All Access); and the wife has her eye on some Peacock shows.

Besides, AT&T’s Stephenson is pretty leveraged right now just trying to deliver our 5G E (eventually) and figuring out what to do with DirecTV. Getting us new, original content is probably low on his priority list.

With a strong foothold in Europe following the acquisition of Sky and content/expertise available from NBCUniversal, Comcast is moving aggressively with a range of payTV, AVOD and SVOD offerings that include shows/movies that are global household names.

CEO/president Brian Roberts emphasized that his organization is focusing on “the fastest way to get to profitability with the least amount of investment.”

At the same time, Sinclair’s CEO Chris Ripley noted his organization is avoiding wading into the SVOD fray and is focusing on news, sports and localized content.

“It’s going to be a sea of blood,” he said, “with losses for many years to come and companies struggling in a major share battle.”

It can’t really be that bad, can it?

Let’s see, there’s Disney+, Apple TV+, WarnerMedia’s HBO Max, Amazon Prime, Viacom’s BET+, NBCUs Peacock, Jeffrey Katzenberg’s short-form startup Quibi, YouTube, Snapchat, Facebook Watch, Hulu, Roku, iQiyi, Hotstar, ITV Hub, Youku Todou. Tencent Video, LeTV, iflix, Hooo, Viu, Viki, OONA, Eros Now, Voot, Tving, Pooq, dTV, BritBox, Canal +, Sky Go, Crunchyroll, Baidu, Vudu, DirecTV; and the list keeps … growing.

Yes, the content industry is IP-based now, which means people have a world of content available to them … and they’re taking advantage of the best content the Internet has to offer from around the globe.

It’s all because different people like different things–even within the same country.

That’s what makes it a challenge for content developers, producers and distributors.

Some people prefer police dramas, horror films, sitcoms, reality, action/adventure, sports and an endless range of entertainment options.

Even Disney; with a large, attractive back catalog and strong brand recognition occasionally hits a sour note with a film and TV series (honest), which is why you have the opportunity to see reboots and spinoffs among the new series and titles that are released every year.

It’s also why Netflix, with more than 150M subscribers in 190 countries, always seems to come up with so many “new and original” winners all of the time.

Nick Nelson, Netflix former head of product creativity and presently head of product innovation at OWNZONES Entertainment Technologies, has noted that Netflix is more effective and using data at a level he has never seen before. “They’re amassing a competitive advantage with a ton of data around how different content plays in every country in the world,” said Nelson.

He mentioned that additional OTT advantages could be gained by connecting data from the customer acquisition and marketing funnel with the consumption data behind the paywall of the product.

With all of its ecommerce expertise, Amazon Prime certainly knows how to capture and retain subscribers.

The organization has streaming deals in place with the NFL, Premier League soccer and was most recently the biggest buyer of EU films for distribution outside Europe.

As services expand globally, international shows/series will be the key to driving subscriptions.

By 2022, Amazon Prime Video is projected to have more than 178M subscribers worldwide.

While the three firms – Disney, Netflix, Amazon Prime – are the first organizations most people mention when it comes to streaming video, they still lag behind the content people who were born on the iNet.

YouTube has more than 1.8B users worldwide, while Facebook Watch has about 2B users.

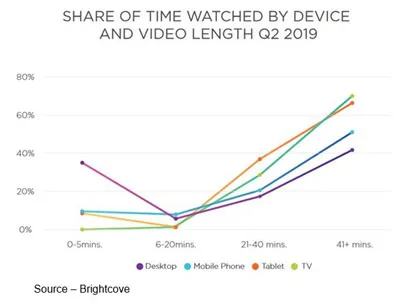

Their Gen Z and Gen Alpha audience moves quickly and easily between TV screens, tablets, computers and phones for their viewing.

Over time, the two could become very formidable AVOD channels. They are already the marketing tools of choice by SVOD services to promote new films, shows, series.

Gross SVOD subscriptions increased to 850M this year and are forecast to continue to grow even as Pay TV subscriptions continue to show modest growth.

China and the US jointly accounted for 63 percent of the global total last year. China overtook the US to become the gross SVOD subscription leader, adding nearly 60 million subscriptions in 2018 while the US went up by 27 million (despite its relative maturity). India nearly doubled its subscription base.

Eight countries had more than 10 million SVOD subscriptions by year’s end, collectively providing 80 percent of the global total.

Greenfled may have believed it when he said folks wouldn’t mind coughing up a few bucks more for so much more “excellent” content; but somehow, we just don’t believe him!

Even as 5G is beginning to roll out, households already have the streaming speed and quality people thought was a distant dream just a few years ago.

Increased broadband speeds allow everyone in the home to stream their content to the screen of their choice, eliminating the need to argue about whose content the family is going to watch.

Instead of gathering around the TV screen to watch a show, entertainment will become a solo experience.

Even if the family happens to be in the same room as the TV set – which occasionally happens in our house – there’s plenty of bandwidth capacity and streaming options

Everyone is doing their own thing together.

As Peter Fader, Wharton marketing professor, called it – fragmentation desocialization.

He sees user-generated content and activities being a major shift in tomorrow’s digital living room using game systems and apps with their avatars interacting with 10-30 individuals from around town, the state, country or around the globe to meet up and create their own reality show.

It’s a concept that Zuck introduced several years ago for Facebook with hundreds, thousands of community groups for friends, family, similar interest folks to get together to discuss, explore, act out and create subjects of common/shared interest.

In a time of fake news, mean/vicious sociopolitical confrontations and intolerance; it may not help OTT services, but the communities could become a less divisive place for people to retreat to and refresh themselves.

Then, they can return to their real world or stream their entertainment.

And here is where the real challenge for the entire industry arises.

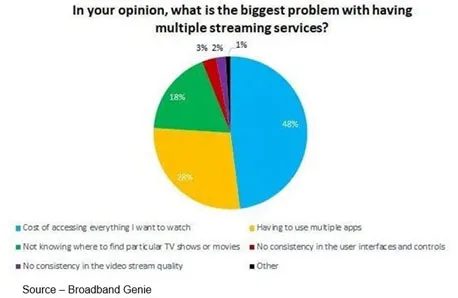

At least at the present time, it isn’t in the best interest of OTT service providers to give consumers what they want – one subscription for their devices with access to the stuff they want to view.

No one really wants to pay for multiple multiple streaming video services.

No one cares how much new, unique content each of the subscription services create, produce, offer up.

No one wants to search one service…then another…then another…simply to locate that movie, show, series.

The industry has forced the individual to waste his/her most valuable asset – time – when the content is available at one single location … even if it is a torrent site.

No one (O.K., most of us) didn’t liked the financial “waste” of paying the less-than-customer-oriented cable guy but the stuff was there when you wanted it!

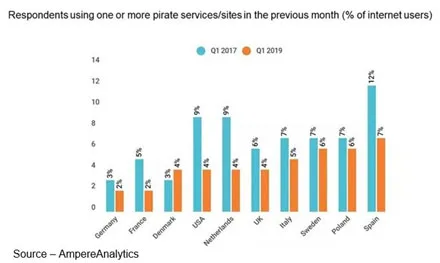

And the brutal fact is that since in today’s increasingly fragmented streaming industry it’s not in anyone’s interest to fully address the consumer’s wants, piracy will continue.

History has shown us that it is not a battle the content creation/distribution industry can win.

The Recording Industry Association of America’s (RIAA’s) attack on peer-to-peer (P2P) came to a head in 2007 when a mother was sued because her son had downloaded 24 songs to her computer. She was found guilty of infringing on music companies’ copyrights and fined $222,000 in damages.

The verdict was overturned but the damage to the industry had been done.

The M&E industry went from a single silo to literally hundreds practically overnight, with each having a self-value of more than the next guy’s.

Sorry fellas, value – as beauty – is in the eye of the beholder.

In this instance, the beholder (consumer) doesn’t value all of the content in everyone’s silos, he/she only values the entertainment they want to watch – anytime, anywhere and on any screen.

Disney has, perhaps, the largest and most valuable libraries and brand perceptions in the industry.

Netflix collects the most useful data on consumer preferences and global appeal. They aggressively and effectively use that data to drive creativity.

HBO has a great reputation among consumers for quality content and a well-defined image of delivering superb entertainment.

And the list could go on but men/women, boys/girls don’t want all of the movies, shows, series in their individual silos.

They want Disney’s Star Wars, Avengers sequels/spin-offs and Lion King, Little Mermaid, Moana futures.

They want HBO’s next iteration of Game of Thrones, Netflix’ next season of Strange Things and Prime’s upcoming Lord of the Rings.

Preferably with a single intuitive interface for the viewer, at a reasonable price with personalized IP, content and recommendations/suggestions.

That’s about it … for now!

Until that’s available to the consumer, he/she will find a single source for their M&E content.

Until that’s available to the consumer, he/she will find a single source for their M&E content.

Queen Gorgo will see what transpired and will observe, “No terms were reached … he was rude, and he lacked respect.”

# # #

Andy Marken – [email protected] – is an author of more than 600 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. Internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields. Extended range of relationships with business, industry trade press, online media and industry analysts/consultants.