The Growing World of Great Content … Now Just Find It

With more than a little sarcasm in her voice, our daughter said, “It’s about time, Tim!”

She was talking about the tvOS, Apple TV announcements she was watching online of the WWDC announcements a few weeks back.

No, she’s not really on a first name basis with Apple’s Tim Cook, but…

The features are “interesting”:

- Dolby Atmos – dynamite sound – on Apple TV

- Zero sign-in

- New TV OS

- Siri support of third-party apps

- Deal with the 2nd largest US cable company, Charter Spectrum

Why is the last item important?

Even if you’ve cut the cord and are OTT, the old cable company’s infrastructure is still best for the last 100 feet to your home screens.

That helps Apple leverage their HomeKit technology.

Smart Tim…smart!

Apple says they’ve sold about 21M Apple TVs and Charter can give them access to about 50M households.

So theoretically, they could finally add the missing link to being a real member of the FAANG

(Facebook, Amazon, Apple, Netflix, Google) and BAT (Baidu, Alibaba, Tencent) gang of major OTT content providers.

Of course, there are a lot of factors we can see that stimulated the change:

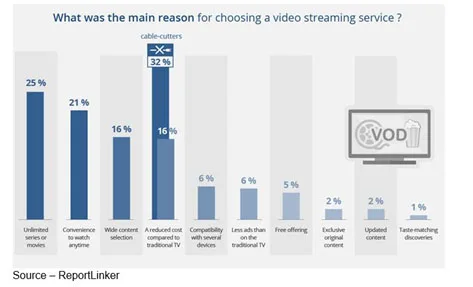

- Rising cost of bad service from cable companies.

- Kids who were born with a smartphone in their hands that they use for everything got adults hooked on the idea and it became the go-to screen.

- Mobile apps provided instant access to the world. According to ComScore, Google and Facebook own eight of the top ten.

- ComScore also found that 51 percent of folks’ total media time is spent in apps.

- Netflix has established itself as the leading OTT service with more subscribers in the U.S. than cable companies, according to PwC

Seemingly overnight (it’s been a couple of years), people got tired of appointment TV and moved to viewing on their own terms.

People who continue with the expensive cable bundle with the hundreds of channels they’ve only clicked past won’t admit it, but habit keeps them connected.

In the U.S., the average cable package is $90 plus. Three plus streaming packages – say Netflix, Amazon, Tencent Video, iQiyi, YouTube, Mediaset, Osn, Eros and the list goes on – cost roughly $40-50.

It’s not only more economic but you can find really unique stuff you didn’t know was out there, and it’s good.

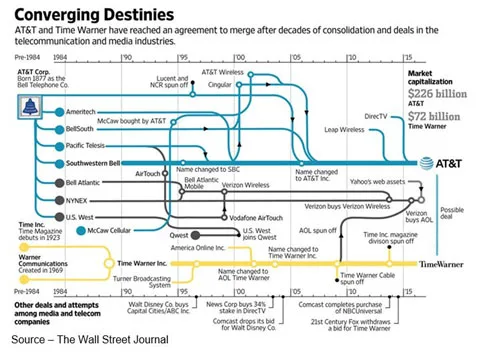

With Netflix establishing major production operations around the globe and signing on some of the best producers’ content, companies and delivery infrastructure folks are rushing into marriages of convenience.

Discovery bought Scripps, Lionsgate acquired Starz, CBS is looking for a buyer, AT&T wants Times Warner, Sinclair bought Tribune, Disney seems to be getting Fox and a good chunk of Sky. Comcast has lust in its heart.

Google, Snapchat, Facebook and Twitter are signing exclusive live event agreements with sport and entertainment venues. Fortunately, one of our services signed on for the FIFA World Cup, so our son was happy.

Around the globe the M&A activity is the same, bulk up to compete in the new streaming arena and we’ll worry about profits later.

All of the action and the thirst for great video content has been good for the economy.

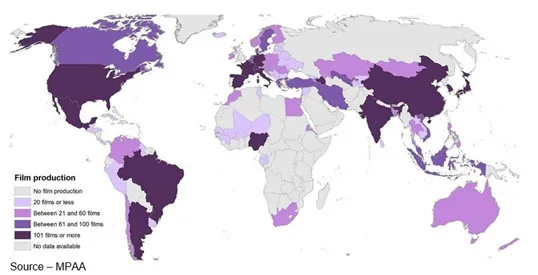

According to the MPAA (Motion Picture Association of America), content production has pumped money and jobs into every country around the world. In the U.S., the industry spent more than $49B with local businesses.

Today, the film/TV industry supports 2.1M jobs. Total wages reached $139 B according to the association, 42 per cent higher than the national average. Production, distribution jobs rose to nearly 700,000.

According to the World Bank, the industry is having a positive impact on local economies everywhere.

Of course it does!

Filmmakers have to meet the demands of thousands of global channels to produce hours of content for billions of screens.

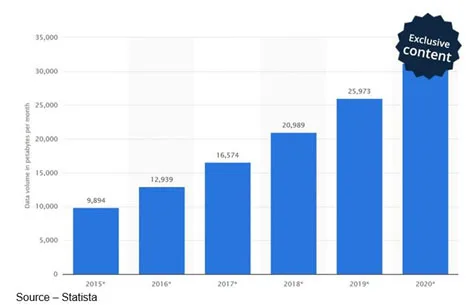

This is great for the thousands of indie filmmakers we know around the globe because they produce trillions of TB of content that have to be stored.

It’s great for billions of people who aren’t zombieized by channel schedules.

Okay, that’s a little unfair because we admit we miss scrolling through the cable system’s TV guide to see what’s on right now.

The volume of anywhere, anytime, any screen content is overwhelming.

It’s estimated that there are more than 200 OTT services in North America, so surfing to find something to watch has become the new level of entertainment.

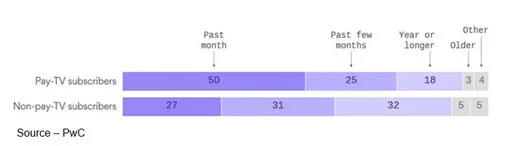

According to PwC, more than half of consumers (55%) look for a new content to watch at least once per week, and 83% look for it a few times per month.

Cripes, we begin the hunt every time we turn on the screen! The importance of migrating content intelligently to each viewer is becoming what “personalization” is all about.

Combining all the viewers interest into a single resource, however mundane, is what the old EPG provided … ease of access, and what is critically in need of today.

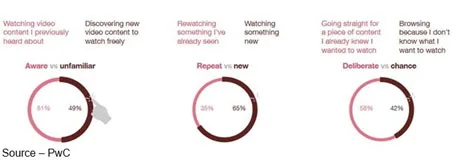

We’re seldom like the one in five PwC found who, out of frustration, rewatch something they’ve already seen.

Nope, we’ll go for something “new,” even if it’s a couple of years old.

Hey, it’s new to us!

Sure, if we stay solely on Netflix or Amazon Prime, it seldom seems to be a problem.

They have mastered the art of user retention by making informed, intelligent recommendations based on what we seem to like, time of day, our mood (not sure, but it seems to be that way sometimes).

We understand that each of the four OTT services in our “viewing bundle” are each intent on user retention; but have you ever wondered what is out there just one click away that will be exactly what you wanted to see?

Yeah, me too.

Can’t wait for someone to come up with an intelligent search function that will streamline the authentication, content curation, personalization and search/discovery part of the entertainment equation.

Until then, folks will have to continue to browse the web to discover new, interesting, exciting content to view.

The problem with that approach is that the content world assumes people know what they’re looking for when they begin the search.

The fact is…we don’t have a freakin clue!

PwC found:

- 32 percent of respondents read a good review

- 27 percent saw an ad

- 44 percent heard about it from other folks

- 87 percent follow the same old TV show, movie they’ve been watching

- 74 percent start something new and know in a few seconds if they want to continue viewing. If not … they’re gone

Cutting the cord seldom cuts the frustration. Until someone comes up with a deep learning solution that addresses your wants and you, it only exacerbates the situation.

Or, as the cabbie said, “Usually I’m not down around here myself, but I wanted to catch that show. That stuff is like gold around here, you know.”

Or, as the cabbie said, “Usually I’m not down around here myself, but I wanted to catch that show. That stuff is like gold around here, you know.”

Most of the time, it’s a fortunate accident.

Maybe it could be another insanely great app Apple will introduce at next year’s WWDC.

If they do, we’ll probably quit hollering “Hey Google” or asking Alexa anything!

# # #