Entertainment Division Delivers More than the Sum

Mark Zoradi and Adam Aron, CEOs of Cinemark and AMC respectively, as well as theater owners/managers around the globe keep exhorting folks to come back.

Producers, directors and actors of the projects have made it a point to enjoy (and talk about) the rich immersive experience of seeing a movie as it was meant to be seen.

We get it and they’re right.

But….

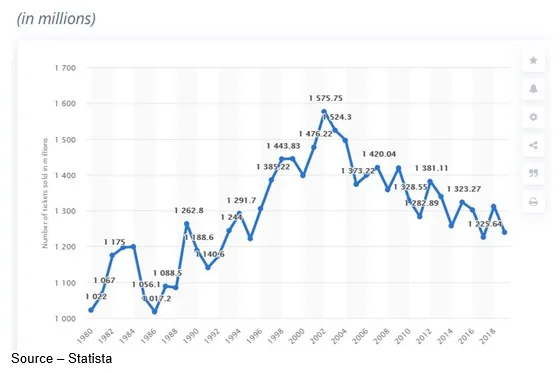

At the beginning of last year, there were over 1,895 thousand cinema screens around the globe.

Five years before, there were 127.46 thousand theaters.

Adding screens and locations would make sense if the industry were growing, but it hasn’t since 2002.

In fact, it has shown a steady decline.

Yes, it’s true, cinema chains have been marginally profitable, but their growth isn’t the result of more seats in seats.

Instead, theaters expanded their concessions…a barrel of buttered popcorn, jumbo sweet drink, a couple of slices of cardboard pizza, burger/fries, boxes of candy that are only a year old, more sugar water and another barrel of popcorn.

BAM! theaters make money.

Then the pandemic hit, theaters closed, people stayed home, and we, like many, changed our video entertainment … forever.

Last year, we upgraded our family room screen to a decent size (55-in) OLED, and we were happy until a friend in Oregon pointed out he had installed an ultra-thin 77-in OLED that took his game play to entirely new level.

Darn!

True, we don’t have the attention span for video games but even they are totally movie-realistic today.

Our screens made the most of our streaming content.

4K with HDR (high dynamic range) makes content really pop and enhanced wide color gamut (WCG) serves up blacker blacks, whiter whites and every color in between is unbelievable.

It wasn’t long before we discovered the sound was … flat.

First, we added a sound bar that provided pretty decent surround sound.

Good, but…

Sound was getting close to the theater experience but as my granddad used to say, close is only good in horseshoes.

Actually, our son was less subtle and said, “The sound sucked!”

What we really wanted was the audio experience we had several years ago at private showing of Gravity at LA’s Dolby theater.

It was one of the first films produced using Dolby Atmos sound technology and was shown in a theater that had Dolby Atmos sound fine-tuned to wring everything possible from the movie.

We never thought about audio until Woody Woodhall, Allied Post, once explained to us that sound is 50+ percent of a movie.

Turn the sound off in a horror movie and it isn’t frightening. Sometimes it’s even laughable.

Turn it off in a high action or sci-fi film and it’s boring.

Thanks to advice from a Dolby friend and a big box tech exec he introduced us to, we had a modest Dolby Atmos surround sound system installed (wife doesn’t trust us with tools).

Viola …

The woman/man cave is more comfortable; the screen is newer, brighter, better; the entertainment options are virtually endless, and the popcorn is way cheaper.

With theaters closed last year in the EU and Americas; large screen smart TVs showed a 9.5 percent CAGR (compound annual growth rate), reaching an estimated $112.4B.

The US market produced an estimated $45.1B in sales with 4K UHD TV sales showing a 9.6 percent increase.

China, Japan, Canada and Europe experienced $27.8B in sales as people spent increased time with at-home viewing.

The pandemic couldn’t have hit at a better nor a worse time for the content creation, distribution industry.

Better

Studios have been “challenging” the 90-day theatrical window for years, hoping to shorten the time between when films appeared exclusively in cinemas and when they could sell DVDs to the consumer as well as monetize the content with short/long-term runs with TV networks.

Previously, when studios were interested in selling projects to and creating works for streamers, they were an unwelcome insurgents in Hollywood.

People like Netflix were looked down on for thinking their films were worthy of prestigious film awards like the Oscars because their work only had nominal theatrical release.

With the successful growth Netflix (200M plus subscribers WW), Amazon Prime (153M plus subscribers WW), Disney + (200M WW) and Hulu (40M plus); studios and networks thought the streaming services might be onto a way to bypass Pay TV and connect directly with the consumer.

Every studio executive team was ready to ease into the ripe D2C market.

Worse

Hundreds of ultra-expensive tentpole projects had been created or were deeply committed to so they would be ready for a global entertainment-hungry market in 2020-21.

They spent tens of million on marketing to whet the appetites of theater attendees.

Thousands of mildly expensive drama, superhero, action, horror and animated films were ready to fill the theaters’ screens between the big budget viewing events.

Modest visual stories had been prepared to attract ticket purchasers to secondary and/or art cinemas.

Suddenly, the doors were slammed and locked.

Suddenly, the doors were slammed and locked.

Hollywood, Bollywood, Nollywood and major content studios around the globe had suddenly stepped into a new era – one with streaming at the center.

Everyone restructured their organizations, activities and workflow. Project priorities and staff requirements were also adjusted.

The result was a hybrid entertainment model which really didn’t satisfy anyone.

Sure, studios still had – or at least gave lipservice to – theaters as an important part of the equation. But more importantly, adjusted the availability and mix of projects that bypass theaters going directly to streaming.

This year will be filled with confusion, name-calling and bashed egos as folks work to carve out their piece of tomorrow.

To get there, we’ll have to significantly improve communications with everyone involved and focus on the mutual goal … all good content matters to the viewer regardless of where she/he sees it.

Every filmmaker, actor and production person we know wants her/his best projects to be shown to an adoring audience on the big, big screen with superbly balanced surround, immersive sound.

Every true film-starved fan ultimately wants to experience these works first as they were written, designed, produced to be seen, enjoyed.

If you look back and forward, it’s the big-budget Marvel-esque blockbusters that will keep audiences flocking to movie theaters.

With so many projects scheduled for distribution and shifted multiple times, studios are closely examining which projects have the best major event, pop culture, merchandising and sequel/franchise opportunities to produce long-term content equity … projects such as Warner’s Joker, Shazam, Batman, Dune; MGM’s Bond franchise; Disney’s Marvel, Star Wars, animated projects; Sony’s Spiderman, Venom, Bad Boys franchises; Universal’s F&F, Minion, Jurassic franchises and Paramount’s MI, John Wick, Matrix series.

In other words, those visual stories that have the greatest potential in putting film fan seats in seats around the globe.

Non-franchise films will fill the gaps in the theatrical calendars; but many – including Oscar contenders – will be with shortened exclusivity windows or day/date releases to their or partner streaming services.

Spin-off superheroes, significant dramas, sequels/prequels and event films and series will be fed to domestic and international streamers to retain and increase subscribers.

Interesting, impactful lower-budget and sometimes so-so films that appeal to the broader audiences will move to streaming services as people increasingly expect a broader range of outstanding entertainment on their new home screens.

The growth will come from a growing mix of PVOD exclusive films, SVOD and AVOD services.

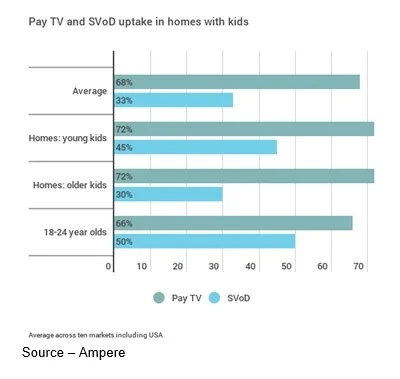

In the Americas, households with seven services are increasingly the norm as people choose services that are cost-effective, flexible, have a range of entertainment options and provide a fast, easy user interface.

Some contend that the subscription to so many services puts the household’s entertainment cost at or above the cost of Pay TV…true!

Others say it is actually more economic when you add in the home availability of theatrical content.

For example, the combined cost of Netflix, Disney +, Hulu as well as Peacock + and HBO Max plus Tubi and Pluto AVOD services is about $50.

That’s about what you would have paid for Pay TV or about what you would have paid to see one film at a theater.

And you can watch what you want, when you want, as many times as you want!

SVoD services tend to be more expensive in the U.S than in other countries and in SEA, there are more subscribers to AVOD services.

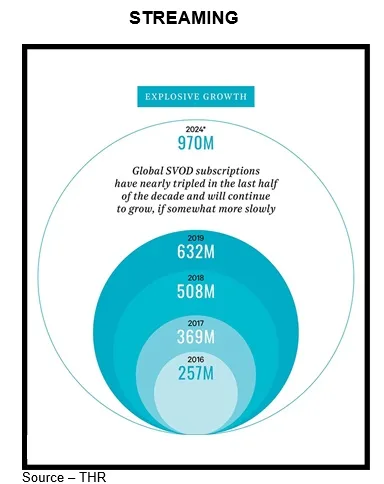

Despite this, SVOD revenue from 138 countries will top $100B by 2025, double that of last year.

Consumers in 16 countries will spend $1B per country with Netflix, Disney+, Hulu and Amazon Prime leading the streaming race globally.

SVOD subscriptions will increase by 529 million through 2025 to 1.17 billion.

China and the U.S. together will account for 51% of the global total with rapid growth in other countries.

The entertainment industry will continue to have the special datenight venue for the “something really special” as well as the solid entertainment venues for the times you simply want to relax.

People will increasingly return to the theater experience.

Serving both of them will be creative filmmakers/teams coming together to give people some outstanding, welcome change of pace opportunities.

As David Rice said in Jumper, “Two superheroes joining forces for like, uh, a limited run.”

As David Rice said in Jumper, “Two superheroes joining forces for like, uh, a limited run.”

And, as the industry becomes comfortable with its new normal … that’s what it’s all about!

# # #

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. He is an internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields. This has led to the development of an extended range of relationships with consumer, business, industry trade press, online media and industry analysts/consultants.