Steaming Needs an Intelligent Search Engine

Don’t you just hate it? You go into the family room and turn on your big-screen set so you can watch a certain movie or program

Suddenly, you have absolutely NO idea which of your paid and ad-supported services it’s on and end up watching something, anything.

We recently read a Deloitte study that found 84 percent of consumers reported they are spending more time with their online entertainment at home.

Well, Yeah!

We’re not atypical. Have a film/show we really want to watch so we cruised Netflix … not there. Moved on to Disney +…then Amazon Prime…then HBO Max and; just for the heck of it, tried Apple TV+.

Bummer: but we really want that film now, so we try our free services … Pluto and Tubi.

Note: Your services will probably vary depending on where you live and your entertainment taste/financial budget, but the big hunt isn’t any different, is it?

Back in the ‘50s, TV enticed families to enjoy the convenience of staying home and watching a well-ordered schedule of movies/shows, each strategically planned by some arbitrator to build the audience. Really hot (sure thing) projects led into others that needed audience exposure.

Lots of folks wondered why go to the movie theater when it will be right on our channel(s) sooner or later.

Folks added one channel after another because no one service had everything they wanted. Soon, it became overwhelming.

So, the cable guy said don’t worry we’ll give you everything you want – 100s of channels for a modest fee and we’ll throw in a neat program guide so you can figure out what is where and when.

The channel numbers went up, the content offering went up, the cost went up and the service went down.

You went to the movie house less and less because TV was so easy to watch and getting out of your cable contract was like escaping from Alcatraz … way too much work and the water outside was deep, dark, freezing.

Eventually, the price outweighed the benefits.

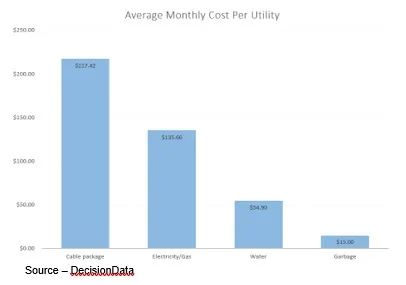

Decision Data recently reported the average cost is $217.42 per month.

The red envelope guy – Reid Hastings – didn’t set out with the idea he was going to take on the cable guy but very simply give people access to films/shows (many of which were only available on DVD); when they wanted, where they wanted and on the screen they had handy.

Viewing was instant and for $8 in 2011 you could watch show after show after …without any bothersome ads until you fell asleep with the remote in your hand.

Susan Wojcicki had already talked her Google bosses into letting YouTube get in on the act and Amazon’s then-CEO Jeff Bezos thought adding streaming video to his book, game and audio services would make the company’s Prime membership look even better.

Studio execs saw an opportunity to bypass the theater owners’ and TV network split so they took back all of the movie and TV deals they bragged about to Wall Street and said their stuff (new and in the library) was so valuable, so in demand that they could charge a premium for their service.

Netflix and Amazon cranked up their own production budgets and schedules.

Last year, Netflix released 129 projects worldwide in the 3rd quarter and the same number in the 4th quarter.

Amazon didn’t say how many new video stories they released in the same period, but they were also a little busy wrapping up the deal for MGM for $8.5B which includes one of the most revered libraries in the industry which includes such iconic titles as James Bond, Rocky, Silence of the Lambs, Legally Blond and more.

Apple, the “gentle giant” valued at $3T, is often overlooked because of its modest roll-out of beautiful content but it surprised everyone during the Oscars in taking away the Best Picture statue for CODA.

It was a first for a streaming service because CODA was also the first streamer movie that didn’t appear in theaters before it was streamed.

Streaming was legitimate!

Studios and networks around the globe like Disney, Warner/Discovery, Sky, BBC, Paramount, Peacock, France24, and more offered their bigger, better services, each knowing their content was more valuable than the other guys’ and therefore should be a value at just “a little bit more.”

In North America, the average household streaming service budget was $55 and home internet connection was $61 (streaming stuff needs the pipe to come to your screen).

Suddenly, that “less expensive” home entertainment service was costing $116 a month–way less expensive than the cable bundle ($217.42) but still…

People had some options – go to a pirate site and download your content along with all of their malware, system hooks, etc. or simply share service passwords with your friends, neighbors.

Going to pirate sites is downright stupid.

With the other approach, the rest of us subscribers, directly or indirectly are subsidizing those who want the content but don’t want to pay for it.

They’re both wrong.

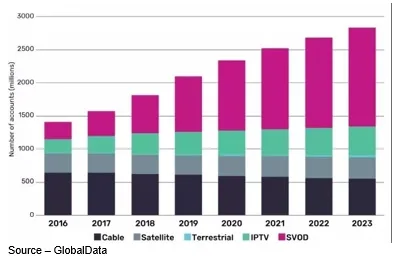

It’s true, SVOD damaged the profits of the cable bundler but there are still more older folks than Gen Z/Millennials, so TV bundled services are still doing OK.

There were about 1.1B subscribers at the end of last year, but the bundlers can see the high profit years are behind them.

That’s why you see the networks greenlighting fewer new series and hanging onto the proven shows.

To fill in the schedules, they add reality TV, dumb sitcoms that went on forever and cop/fire/med stuff while the subscription folks roll out a steady stream of very good and OMG content that appeals to people emotionally, intellectually or simply lets them sit back and watch.

It’s true.

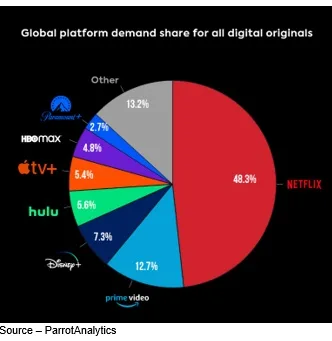

Today, some of the best content in the world is as close as a few clicks for us since we have the best five subscription services (our opinion) available and the two best ad-supported services.

That also means we have too many video streaming services. We come for the content and leave for the cost just like households around the globe.

Well, you don’t exactly leave; you drop one service and pick up another that has more of the content you want.

And later probably return.

It’s a little like the pony express in the old West. Ride a horse – hard – for a period of time and then jump onto a fresh one and continue your entertainment journey.

Of course, like the horse you left at the station, it’s not that you disliked the subscription service, you just wanted “a change” to something “new,” “fresh,” “different”.

On your return trip, you find you’re getting tired of that new horse, so you jump onto the horse you left awhile back and ride on happy with the new/old service.

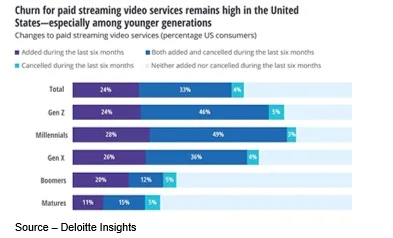

In the entertainment and communications industries, it’s called churn where you drop one service for another and then later reverse the process.

It’s far from new – the phone guy has seen it for years – and it costs streaming services millions because it’s more difficult to recoup their subscriber acquisition costs.

The old rule of thumb was that it cost 5x more to get a new customer than to keep an existing customer. That’s because streamers must build new content from the ground up to personalize it and appeal to a new subscriber.

The cost could be as much as 500 percent greater.

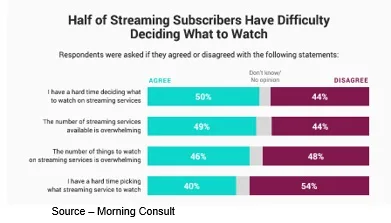

Over the past few years, we’ve discussed this issue with Allan McLennan, CEP/Media, Head of M&E North America, Atos, multiple times and he always points to the same issue. “Consumers are overwhelmed by the sheer volume of content from streaming video providers and are increasingly frustrated with the efforts needed to access it.”

Growth for the major North American subscription services like Netflix, Amazon, Disney, Warner/Discovery, Paramount and even Apple has slowed, which is why they have expanded their scope to the global market with new local and regional content as well as their exported projects.

In the past two years, subscribers have become increasingly frustrated when they lose content on one service, have to juggle multiple subscriptions and have the service’s recommendation engine serving up poor or meaningless viewing options.

McLennan noted that studies have shown that churn has held steady at 37 percent for paid streaming services as people subtract/add services in search of content they want and 25 percent return in 6-12 months for the service’s new unique content.

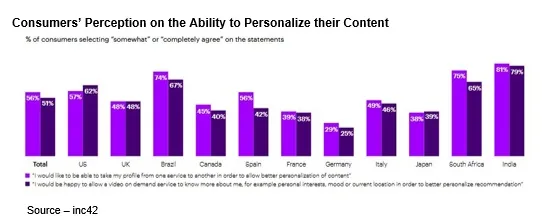

“Netflix deep data analysis has shown that consumers are more than willing to share their personal information with their streaming service in return for being able to manage and search for movies/shows they’re interested in or might be interested in,” said McLennan.

“But even they know they have to constantly improve and refine the service to improve their retention,” he added. “And most of the other services are just beginning to realize that simply adding new projects to their service isn’t the solution. They need to earn the trust of their subscribers so they can improve and expand their recommendation data in addition to using the data to greenlight projects that meet the subscribers’ entertainment demands.

“It’s a long, hard and expensive road,” he emphasized.

But that’s still not the solution for the consumer because what folks really want is a service that searches across all of their services – subscription and ad supported – and offers up the movies/shows they might/should/could be interested in watching.

If it sounds a little like the solution of the old cable bundle days … it is.

“As we’ve discussed before, what consumers want is a channel of one,” McLennan stated. “An aggregation service that eliminates all the pain and frustration of the entertainment search.

“In other words, they want a service on top of the services that manages all of the user’s accounts as well as content discovery and recommendations,” he continued. “The company that comes up with the solution or the services that join forces to offer a singular one-source solution will deliver the entertainment value people really want.”

Of course, that service of services will make it difficult for outsider as well as mid-sized and smaller streaming services to compete but there’s always the merger route–survival of the service(s) with the deepest pockets or ready access to funds.

Who knows, maybe the bundled service will be better the second time around.

Of course, for the content creation folks, Kofuku’s observation in Drive My Car seemed to have the right attitude when he said, “From a social standpoint, that’s not good. But it’s not necessarily a drawback for an actor.”

Of course, for the content creation folks, Kofuku’s observation in Drive My Car seemed to have the right attitude when he said, “From a social standpoint, that’s not good. But it’s not necessarily a drawback for an actor.”

The consumer is happy, the bundler is happy, streaming services are happy. What could possibly go wrong?

# # #

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.