SVOD Growth Based on Greenlighting the Right New Content

There’s a ton of good/great content out there.

Every streaming service has some; but when you sit down in the evening, which service and which show/movie do you watch?

Do you just let the service recommend the one it’s pretty sure you’ll like?

Or do you check out Rotten Tomatoes or a publication’s “here’s what’s hot” list?

Not us, boy… we received a solid maybe recommendation from a friend awhile back:

“Here’s a Sci-Fi movie I can recommend. It’s somewhat derivative — but still worth watching – a bit like Inception or The Matrix but still original enough. The special effects are great – almost spectacular – even if the acting isn’t top-notch – and on the surface, it appears to be somewhat incoherent.”

Oh yeah, it was okay, but we like beyond reality stuff.

The key is that studios, the old folks in the content creation industry – Disney, Warner, Discovery, Paramount, Peacock, Sony, Lionsgate, Legendary, and those in production centers around the globe – quickly realized that the upstarts – Netflix, Amazon, Youku, IQiyi, Salto, Britbox, Viaplay, RTL and folks in every region – had a good idea going direct to the consumer.

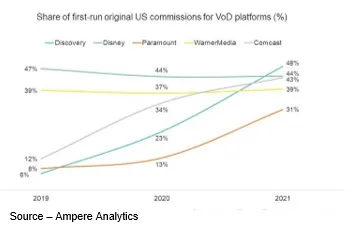

According to Ampere, nearly 50 percent of the new content the studios/networks produced last year was delivered to their streaming services–all to entice new subscribers.

And it worked.

- Paramount+ (ViacomCBS) racked up 56M

- Disney+ (including Hotstar) reported 118.1M

- Hulu (60 percent owned by Disney) had 40.9M subscribers

- Peacock (NBCUniversal) 24.5M

- HBO Max (Warner – now “bundled” with Discovery) totaled 73.8M

- Discovery (before taking in Warner) 22M

That was good news for producers, directors and crews because it means the pipelines will be filled with projects and there’s no end in sight.

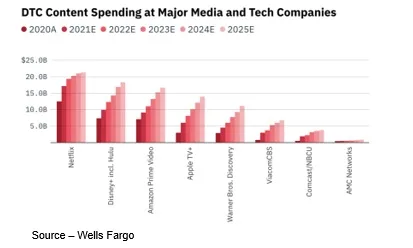

This year, the industry is expected to invest more than $230B.

They even had visions of “owning” the viewer until they found out that the ungrateful folks would slip away once they had seen the new stuff.

While the U.S. global hopefuls will be investing in content, they won’t be alone.

There are a number of regional providers who are also setting their sights on viewers at home as well as overseas. NHK, Tencent, ARD, Baidu, France TV, Canal+, Telefonica, BBC, Alibaba and more are all investing in original content to win new customers.

The content-rich vaults of Disney, Warner, Paramount and other studio/streamers have been widely touted as the old guys’ secret sauce, yet it’s the new, exciting stuff that gets people to subscribe.

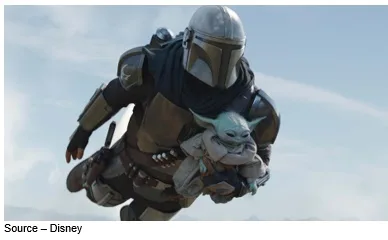

When Disney+ was rolled out, they didn’t lead with Star Wars, Indiana Jones, Apple Dumpling, Hanna Montana, Jungle Book and thousands of films/series that are carefully stored away in their vaults.

Nope, they hit the market with something totally fresh, totally different.

They took their lead from Netflix that showed the market that telling the subscriber there is something new and unique would make folks want to sign up.

Still, even Netflix found that libraries can be useful if you use the subscriber data to determine what folks are watching and how long they’re watching and then analyzing why they might be viewing old stuff.

And for the younger online audience (14-34), they’ve racked up an impressive library of the older comfort food to keep them involved along with the edgier new content.

Netflix behavior data analytics has enabled the company to develop 2,000 different homepages for a wide range of taste groups to give them a personal home base and content of interest selection list tailored just for them.

Reboots, spin-offs and plot extensions were greenlighted because it was apparent there was a substantial market for the renewed content.

It was something Disney used–a proven commodity when they rolled out their service not with Star Wars but with something new and different yet enjoyably familiar – The Mandalorian.

Following the acquisition of MGM and its rich library, Amazon’s Andy Jassy said the company gained a lot of insight using advanced data analysis on both the new content and library views.

Using advanced data analytics, the organization was able to develop data about actors, TV shows and movies that helped them develop a strong balance of new and revived content to expand their audience to 200M plus this year.

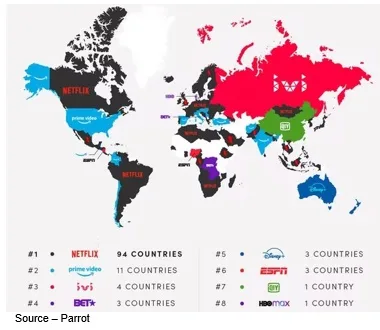

To maintain its continued growth, Netflix – and to a lesser degree Amazon – has focused on extending its reach, especially in Asia and Latin America, and has production centers across the world including Spain, France, Germany, Brazil, South Korea and more.

SEA and EU countries require that 30 percent of content be local work, but Netflix has found an added benefit beyond lower-cost production.

It has led to their developing significant growth in South Korea because there is local content, but it has also produced international subscriber interest as Squid Game quickly became popular around the globe.

The same is true in Japan and elsewhere internationally as anime became the content of choice by the younger audience.

While Europeans enjoy well-subbed and dubbed content from the U.S., subscribers in other countries gravitate to a variety of content from around the globe.

Netflix officials at this year’s MIP TV event noted that every country has a different adoption and interest curve as well as pricing sensitivity point.

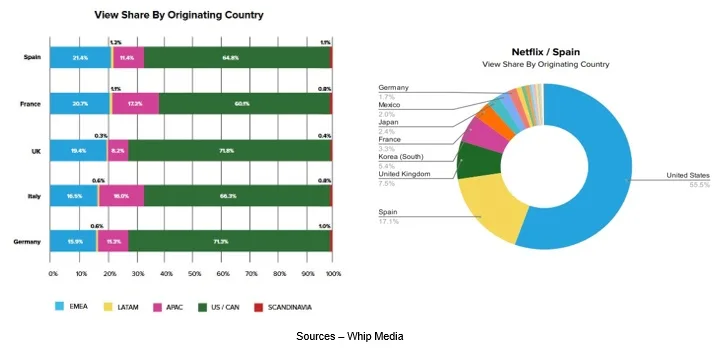

Take Spain, for example, where people quickly signed up with Netflix for La Casa de Papal which also gained significant viewership in other countries, especially in the Americas as The Money Heist.

Whip Media officials reported that US content had declined more than 10 percent as subscribers in France, Italy, Germany, the UK and Spain chose localized content viewing.

The good news for Netflix (and Amazon) is that the content also appeals to global subscribers.

All of the streamers – Disney, Warner/Discovery, Paramount+ and Peacock–want to be major global players.

Disney itself is juggling more than 300 local-language productions to grow its international subscription base with local content.

Obviously, all of the studio/streamers want to uncover what Netflix unveiled – Squid Game and The Money Heist – local content with global interest. However, the only global player right now is Netflix, and they have the proven access to the highly sought-after commodity … talent.

Netflix is rolling out original content from Turkey, Argentina, Mexico, New Zealand, Sweden, Denmark and other countries, including more than 20 originals from Korea.

In addition, because of their years of experience in the streaming field and seemingly uncanny way of picking winners (it’s the data), Netflix and Amazon are in a good position to improve their subscriptions globally in a market that has yet to reach saturation.

VOD subscriptions are projected to increase 108 percent to 1.6B by 2026.

But according to Moffett Nathanson, the expansion for potential in the Americas is only about 6.7M households. New potential customers in EMEA are 84.5M and 80.1M in Asia which include a major dose of less-affluent countries where mobile devices are the primary source of communications and entertainment.

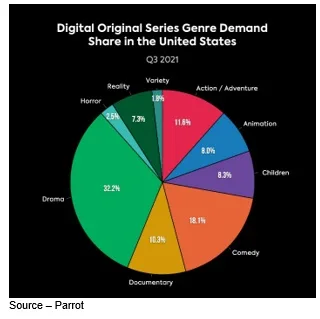

The thing that all streamers – especially studio emergents – have to do is develop the best balance of content in the basic genres.

- Action

- Comedy

- Drama

- Fantasy

- Horror

- Mystery

- Romance

- Thriller

- Western

Content country of origin, genre and steady subscription growth are difficult to balance and frankly, more experienced luck than scientific fact.

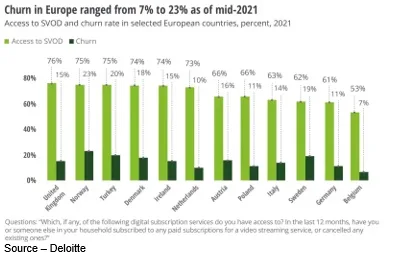

What we always find amusing is Wall Street’s reaction to quarterly subscription increases and churn (losses).

We have four pretty permanent subscription services, two AVODs and one in/out SVOD – if our “permanent” services get too aggressive with their fee increases their status may change.

What’s an in/out service?

It’s a streaming service that could be almost any of the others that we sign up for based on new, interesting films or shows that we stick with three-four months or until something newer, more interesting comes along and then BAM! we’ve moved on.

Deloitte recently predicted that 150M folks would cancel a paid subscription but unless that subscriber is deceased, they could – and probably will – return … sometime.

Deloitte recently predicted that 150M folks would cancel a paid subscription but unless that subscriber is deceased, they could – and probably will – return … sometime.

As George Hanson said in Easy Rider, “I mean, it’s real hard to be free when you are bought and sold in the marketplace.”

The biggest problem for the heads of many streaming organizations is that they view the streaming market as an almost exclusive goldmine–they get the gold and the consumer gets the shaft.

Just doesn’t work that way today.

Streaming services have to continually work to select and develop content for their subscribers and balance that with a monthly subscription fee that the consumers feel is equitable.

When it isn’t, consumers get on their bikes and ride!

Something is better down the road and maybe – just maybe – folks will come back around and stay for awhile.

# # #

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.