OTT Producing Excitement on the Screen, Behind the Scenes

Anand Sanwal, CB Insights CEO, constantly reminds organizations that the most difficult decision management has to make is determine it’s time to change direction, replace/kill their best product line because the world is changing; and if they don’t do it, someone else will (https://bit.ly/2KyO3zw).

When you scroll through the list of 59 quotes, the missteps are painfully, humorously obvious; and you can draw a strong comparison with the shift that is taking place in the M&E industry.

While cable TV is still the entertainment industry’s cash cow, customers around the globe are cutting/shaving their cords.

The cancellations of traditional video service subscriptions and declines in viewership are depressing advertising growth, according to Michael Nathanson, of the MoffettNathanson analyst firm.

He projects flat advertising spend for the quarter — including a one percent gain for cable (to $5.6 billion) and one percent decline for broadcast (to $3.2 billion) and added that cable’s C3 ratings (commercial times during programs) declined by 14 percent and networks by nine percent.

If that wasn’t bad enough, the quarter could be the weakest on record for cable networks’ affiliate fee growth (four percent, down from six percent), even though retransmission fees were still healthy.

No wonder he summed up his entertainment industry analysis by saying it was “freakin’ ugly”.

He did his darndest to highlight a few bright spots but still he only had one piece of advice for participants, “Man the lifeboats!”

If that wasn’t bad enough, Marty Shindler, who tracks the theatrical scene noted that year-to-date box office receipts were off 6.2 percent for the year.

Unless you’ve been sleeping under a rock, the reason is obvious … streaming.

Allan McLennan, PADEM Media Group’s Chief Executive, explained entertainment and tech firms are stepping up to compete with the middlemen (cable system operators, multiplex chains) and preparing to sell content directly to the consumer.

The result?

More venues for films and thus beginning to be fewer films in theatres, starting to drive reduced release windows, ultimately less content for traditional TV and increased branded relationships with viewers.

Every must-see show – Disney’s The Mandalorian, Forky Asks a Question; Apple TV +’s See, The Morning Show; Netflix’s El Camino, The Ballad of Buster Scruggs; Amazon Prime’s Good Omens, Hot Fuzz; HBO Max’s Doom Patrol, Dune: The Sisterhood and a growing string of great content are featured in the OTT offering to entice new subscribers.

Traditional players like Disney and NBCUniversal (Peacock) that have major cable nets understand that at least in the near term, it will mean reduced ad sales and more difficult fee negotiations; but they also realize that it is best to be effective players in both arenas over the long haul.

There are already more than 270 streaming services in the US and globally more than 1,000–all committed to capturing a major portion of consumers who want new, original and unique content.

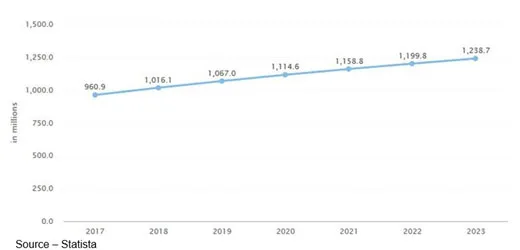

There are more than 500M OTT subscribers this year and combined, the leading online video services (Netflix, Hulu, Amazon Prime) represent more than half of the pay TV users.

SVOD will represent about $24,771M this year with an annual expected growth of 3.2 percent and most of the revenue generated in the US ($11,420M).

User penetration is 14.5 percent this year and should hit 16.2 percent by 2023. Average revenue per user is $23.22.

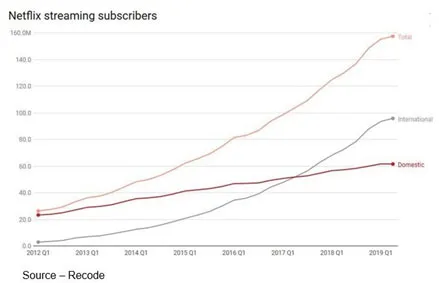

Netflix started the content shift back in 2007, when it began streaming movies and TV shows and has expanded its viewership steadily since then by spending $12 billion this year on programming.

Focused on creating interest and demand for all of the OTT services, the company has captured more than 166 M subscribers worldwide.

With international subscriptions of more than 95.9M, Netflix represents more than 30 percent of all streaming subscriptions.

Netflix and Amazon Prime global growth will continue (Hulu is US only)–especially in developed countries. However, new entries like Apple TV+, Disney +, Peacock and others will slow their US and international expansion.

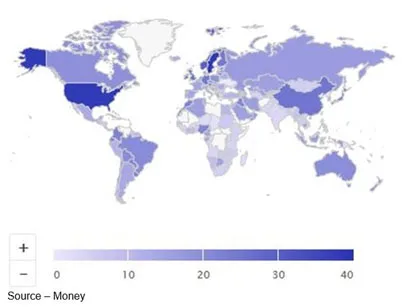

While China represents a huge potential market (1.4B population), there is a general lack of interest by the streaming services in dealing with bureaucratic issues when there is so much potential in the other 192 countries around the globe.

This leaves Chinese consumers with three choices – the iQIYI (backed by Baidu), Youku-Tudou (backed by Alibaba), and Tencent Video (backed by Tencent).

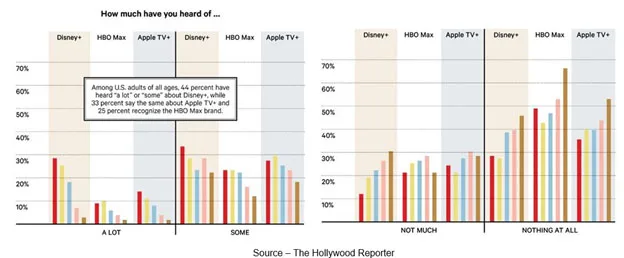

While the new streaming services are household names for folks in the M&E industry, that isn’t necessarily the case for the potential subscribers the services are looking to sign up.

Despite some minor hiccups, Disney+ signed up more than 10M people for its service the first week.

“TV/basic cable gets the proverbial leftovers,” McLennan added.

Apple is anticipating/hoping that its market of more than 100M device users will choose Apple TV + as one of their mainstay streaming services.

Meanwhile, Netflix may experience a temporary loss of US subscribers, but their international growth will make up the difference and unique content could bring people back into the fold.

Since Amazon provides users “added benefits” few people that are subscribers will probably not disrupt their relationship for a different streaming service.

AT&T’s WarnerMedia and HBO Max are working to ensure they continue to be a major streaming participant.

HBO already has 34M subscribers and AT&T says it wants 50M HBO Max subscribers by 2025.

To jumpstart the service, AT&T is giving the service to its premium unlimited wireless subscribers and top-tier home broadband customers and could offer its 160M mobile customers other free streaming services to ensure their growth and market penetration.

Disney’s Iger is determined to leave a strong legacy when he retires in two years and said at the launch, “We’re all-in!”

The company estimates the service will have 60-90M subscribers by 2024, thanks to its robust Marvel, Star Wars, Pixar, National Geographic, Hulu, ESPN Plus, Hotstar, Fox studios/library, a strong family-centric global brand recognition and a refined consumer-oriented marketing machine.

“We were now hastening the disruption of our own business,” Iger wrote in his memoir, “The Ride of a Lifetime.”

To emphasize the Mouse House’s need to change, he entitled one chapter, “If You Don’t Innovate, You Die.”

The streaming revolution has only just begun, according to McLennan; and it’s going to change everything.

“So much change is happening so quickly that viewers are in the process of becoming overwhelmed,” McLennan commented, “and not all in a good wa. Some viewers are starting to think the cable bundle in many ways is more manageable by comparison.

“Cable’s greatest challenge is overall cost, with new IP platforms starting to provide them with to be more competitive,” McLennan noted. “These businesses will coexist. It’s not like everyone will migrate to the new OTT offerings at the same time.”

Cable has “comfort” on its side offering familiar programs, access and channels with distinctive identities he noted.

That familiarity is what the streamers are counting on:

- Disney + is launching with more than 620 movies, more than 10,000 TV episodes and countless shorts, features.

- HBO max will have 10,000 hours of programming including Friends, The Lord of the Rings, Gossip Girls and new shows.

- Peacock will offer 15,000-plus hours of programming including The Office and new shows.

- In addition to its global subscriber base, Netflix has a growing library of originals that can be refreshed in the years ahead.

The services increasingly use audience analysis to determine if they have the right mix of genre, themes, mood, release type and subgenre to appeal to the widest possible audience at the outset.

They then use their growing database of viewer information to fill in holes or develop content to reach new subscribers and reduce churn.

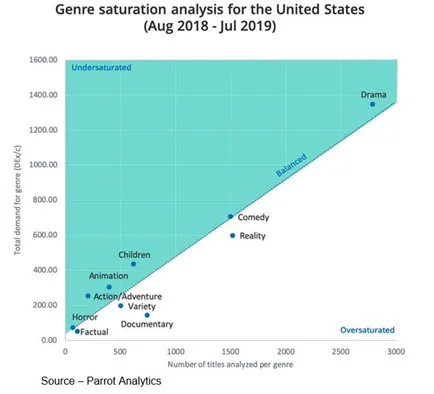

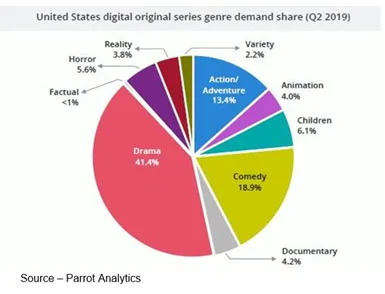

Reality shows, documentaries, factual shows, variety shows and horror shows appear to already be oversaturated genres in the US; but organizations target talent based on their specific genre needs:

- Dramas, comedies have enjoyed the largest US demand

- Children’s content, animation, action-adventure show room for growth

- Comedies have a good balance of availability/demand but still have room for growth

As a result, the biggest changes that have taken place with the onslaught of streaming services have been the rush for focused talent and content ownership.

Netflix, Apple, Amazon, established studios, TV networks and well, just about everyone have been aggressively poaching writer-producers, showrunners and pivotal talent to develop/deliver content that will meet specific viewer tastes.

Even by Netflix standards, the paydays have been eyewatering as providers dig deep into their pockets for the increasingly scarce talent.

Major names with track records in specific genres and subgenres have been pursued with the hope that they can deliver content that will produce an uptick in subscriptions.

Because of the significant demand for new and unique content, cable and OTT services are making major investments in people, ideas and scripts at all levels.

However, it is a mixed benefit for most indie filmmakers, writers, shooters, editors, FX specialists and audio specialists.

Streaming services are ordering fewer episodes and canceling series after shorter runs, so the pressure to switch from one project to another can be increasingly stressful, nerve-wracking and financially unsettling.

In addition – and more disturbing to creatives, there is a seismic shift in employment contracts.

Popularized by Netflix and now being implemented by Disney, Amazon, Apple, and others; higher upfront payments are being paid with little or no back end.

The shift gives the OTT services and now the traditional theater/TV service organizations greater flexibility on where, how and when content is shown.

In many ways, it’s an effort to take a page from the old studio system – buy the content creation team out up front so they don’t have to share profits over the life of the project.

As one member of the creative community observed, “Bottom line is that they will never have to tell us the truth about the value of our content.”

Of course this could change, because the US justice department wants to overhaul some of the ancient studio rules (https://on.wsj.com/37eRNQt – subscription).

Looking at the move as something positive, Max Kenton said, “Charlie, I think there’s a whole robot in there!”

After all, the M&E industry is supposed to be something everyone can enjoy!

# # #

Andy Marken – [email protected] – is an author of more than 600 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. Internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields. Extended range of relationships with business, industry trade press, online media and industry analysts/consultants.