Streaming Video is Evolving

Some people don’t take bad news real well.

Take Netflix for example.

They lose a couple of North American subscribers – 1.3M to be exact – and financial/security analysts say the golden boys (Hastings/Sarandos) have lost their touch.

And they’re not real sure about the other streamers either.

Really?

Look at the available market:

- 5M TV homes in the US – Statista

- 122M homes with broadband connectivity – cable/fixed wireless – Kagan

- 60M Pay TV households ($100+ bundles) – Nielsen

- 1M (16 percent) of population 65-plus (US Census)

- 20 plus video streamers including the big boys – Netflix, Disney, Amazon Prime, Hulu, HBO Max/Discovery, YouTube, Peacock, Apple, Pluto, Tubi, etc. – competing for $35B market – Statista

- 7 services (SVOD, AVOD, FAST) average per household – Kantar

Yeah, it’s a big market, with big players and growth is getting tougher … for everyone!

Unlike a few industry bosses, Reed told his people what was going on, “Both Ted and I regret not seeing our slowing revenue growth earlier so we could have ensured a more gradual readjustment of the business.”

For folks who can’t translate that, it means they’re firing in some areas, adding in others, tweaking the organization and other stuff.

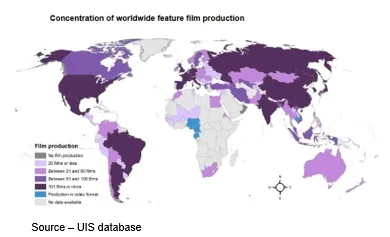

North America may be the biggest streaming market but it’s not the only place folks make/watch content.

Netflix, the only true global streaming video service, produces content in 190 countries in Europe, MEA (Middle East/Africa), LATAM (Latin America), and APAC (Asia – Pacific) for local, regional and international audiences.

Of course, they’re not alone in their ambition. Disney moved ahead of Netflix with 221.1M subscribers, Disney +–152.1M, Disney+ Hotstar–58.4M and ESPN+–22.8M. They also own 2/3 of Hulu (may buy the rest from Comcast)

Disney plans to have branded SVOD service in 150 countries by the end of the year.

An integral part of Netflix and Disney+ growth is that they don’t think of “international” as an export market.

In addition to the fact that to stream content to a country’s citizens, Netflix (and all streaming services) had to produce 30-40 percent of their content library locally.

Netflix quickly learned what Disney has known for years, “great stories can be made anywhere and loved everywhere.” The company has built out its creative development, personalization, and language presentation/localization around the globe.

Netflix is presently producing film/TV shows in more than 50 countries, resulting in strong service/content audiences locally as well as internationally.

Netflix’s Sandaros noted that the firm has dramatically broadened its pool of content to creators to include indies to serve local tastes and expand its content variety globally.

Research at Purely Streamonomics’ found that indie content spending jumped 25.3 percent year-on-year over the past two years and now accounts for 65.5percent of the world’s film and TV production activity.

“To continue their user growth, the two – and most SVODs – are leaning into the fact that ad-free is ‘fine’ but people will consider AVOD/FAST options,” said Allan McLennan, CEO/Head of M&E Industry, PADEM Media Group “People are developing a value equation for their entertainment budget; and if they can find what they’re interested in respectfully managed FAST-based offerings, they’ll consider it,”

Consumers who are willing to pay more for ad-free viewing place more value on content availability, exclusivity, search, discovery and the user interface.

“There are services they go to regularly for their entertainment and others they would like to have as long as the cost is right, both economically as well as the amount of commercials injected,” he added.

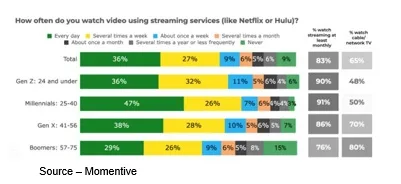

According to Momentive Research, more than 2 in 3 (68%) U.S. adults would choose Netflix as their first choice across all age groups if they could only choose three services. Disney is second with Gen Z and Millennial subscribers while Prime Video is second among older viewers.

Disney and Netflix are both developing AVOD and FAST options and pricing tiers which will be introduced late this year to supplement their user bases and supplement their bottom lines with ad sales.

“People are comfortable with ads as long as they’re relevant and limited,” McLennan noted, “by properly using subscribers’ data they can help advertisers ensure their ads have the right balance of meaningful ads without being abrasive or overly intrusive.”

“In addition,” he continued, “it will enable them to get a solid foothold in the $65B plus annual TV ad spending that is slowly moving to streaming and positive for the overall television industry.”

Ad industry executives are very interested in learning more about the marketing opportunities – and cost – for the two leading streaming services.

McLennan said the two will probably tip-toe into their ad-supported activities with perhaps four minutes of commercials per hour, varying pod lengths and different ad schedules/ads for episodic content and feature films.

“They will probably start with 15-30 second spots and then evolve their program as they learn how people come online and use the services,” he speculated.

“Ad pads and options – pre/post roll – will undoubted increase,” he added, “but we don’t see them ever getting to the unbearable 20-minute ad blocks in an hour people experience with pay TV.

“Consumers won’t tolerate it,” he emphasized, “and it’s too easy to move on or cancel a service that gets too greedy and pick up a more viewer-friendly service such as Pluto, Paramount, Tubi, Freevee, Peacock, Roku.”

We know you probably wonder where WBD – Warner Bros Discovery – fits into the mix because they are one of the Big Three – Netflix, Disney, HBO Max/Discovery +…right?

Yes … but!

A lot of the time, they just can’t get out of their own way.

Now waist-deep in the merger, Zaslav has stated that Warner Bros. theatrical exhibition has become a focal point, even as they pulled Batgirl and other films from theater calendars as part of a cost-cutting move and tax write-off, emphasizing that the company will focus on quality and won’t put out a film that doesn’t meet those standards.

However, back when Discovery acquired Scripps Networks, he noted “We don’t do red carpet. We don’t do Hollywood stars. We pretty much don’t have actors. We have authentic talent. We focus on strong brands, passionate audiences and real-life entertainment.”

But that was then … this is now.

A man of decisive action not unlike one of his inspiring business leaders, Neutron Jack Welch, he has focused on slashing content spending, cutting some HBO Max programming and realigning staffs/organizations at Warner, Turner, CNN, DC Entertainment and other content silos.

And it was probably necessary given WBD has a gross debt of $53B in addition to his annual compensation package of $246M and an employment contract through 2027.

The effort for the near term is to free cash flow to support the stock and pay off the debt.

The large cuts throughout the company, especially those in the content creation/production area, have created serious doubts in Hollywood and the movie/TV production marketplace.

The large cuts throughout the company, especially those in the content creation/production area, have created serious doubts in Hollywood and the movie/TV production marketplace.

It will be interesting to see how the company brings together HBO Max (unscripted content) and Discovery + (largely nonfiction) as they shift away from heavily discounted promotions and rely on a subscription fee that is already the highest in the industry, $14.99.

While the wholesale changes may be alarming; as one executive noted, hope springs eternal at WBD.

However, paving over that much history is dangerous for the company … any company.

We’ll just have to see what the new streaming entity looks like and is received when it really rolls out mid-next year.

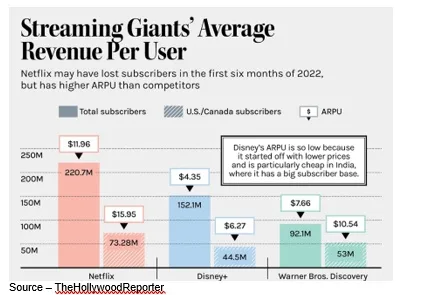

Until then, established streaming services (Netflix, Disney, Freevee, Paramount, Peacock and others) are shifting their attention from subscriber wins/loses to something more meaningful – ARPU (average revenue per user).

The first to focus on ARPU has been Netflix, which is by far the most mature firm in the subscription video arena.

In the last quarter, they reported the highest ARPU with 73M subscribers (North America) of $15.95 per member, EMEA – $11.17, APAC – $8.83, LatAm – $8.67.

Disney+, on the other hand, reported $4.35 per subscriber.

The monthly ARPU will add value to the streaming services’ advertising value (cost), while improving their revenue/cash flow growth.

To continue to increase their ARPU, streaming services should probably consider things like annual subscription options.

To continue to increase their ARPU, streaming services should probably consider things like annual subscription options.

It has worked for years for the mobile device folks.

Maybe sign up for a year and get 1-2 months free.

After all, it costs more to get a new subscriber than to keep an existing one.

And as long as the annual fee is “modest,” folks will stick out of habit just as they have with your mobile phone company … switching is such a pain.

All the streaming bosses have to do is follow Zelda’s advice – “That’s good. Keep that up. Lookin’ like you don’t know anything.” – and things will roll along smoothly.

# # #

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software, and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media, and industry analysts/consultants.