Streaming Services Set for a Major Shift

Back in the day (2017), having a SVOD (subscription VOD) service like Netflix, Amazon Prime or Hulu was a little cool and didn’t cost all that much ($20/mo. total).

You could tell folks in the office all the really great shows/movies you were watching when you wanted to watch them. You could even watch movies that were up for Emmys/Oscars while the Academy squirmed when it had to recognize fantastic video content that was never created to appear on the monstrous popcorn screen.

The special feeling became a little hallow two years later when movie houses shut down and the stuff destined for the large screen had no place to go.

Studios and entertainment giants everywhere took a right turn and went on a massive acquisition, corporate realignment move rushing to get their content in front of families around the Americas, Europe and slowly into APAC households.

The idea that the added convenience and far superior value of content was worth a “reasonable” monthly cost was obvious.

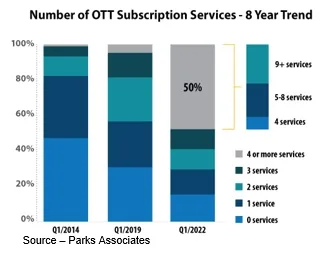

In less than a year, the siloed options became endless. Folks cut their $100+ pay TV budget in favor of endless variety from … everyone.

The options in the Americas are fantastic and they’re just as varied in every corner of the globe:

- Amazon Prime Video: $14.99/mo.

- AMC+: $8.99/mo. or $83.88/yr.

- Apple TV+: $4.99/mo.

- Arrow Player: $6.99/mo. or $69.99/yr.

- Brown Sugar: $3.99/mo.

- Criterion Channel: $10.99/mo. or $99.99/yr.

- Discovery+: $6.99/mo.

- Disney+: $7.99/mo. or $79.99/yr.

- The Disney Bundle (Hulu, Disney+, and ESPN+): $19.99/mo.

- ESPN+: $6.99/mo.

- Fandor: $5.99/mo. (or $3.99/mo. with Prime Video Channels)

- Full Moon Features: $6.99/mo. or $59.99/yr.

- HBO Max: $14.99/mo.

- Hi-YAH!: $3.99/mo.

- Hulu: $12.99/mo.

- Hulu + Live TV/Disney+/ESPN+ bundle: $75.99/mo.

- Midnight Pulp: $4.99/mo. or $49.99/yr.

- Mubi: $10.99/mo. or $83.88/yr.

- Netflix: $15.50/mo.

- Night Flight Plus: $4.99/mo. or $49.99/yr.

- Paramount+: $9.99/mo.

- Peacock Premium: $9.99/mo.

- Philo TV: $25.00/mo.

- Pluto TV: Free

- ShortsTV: $1.99/mo. on US Prime or $65/mo. w/o provider

- SHOWTIME: $10.99/mo.

- Shout! Factory TV: $2.99/mo. on Prime Video Channels

- Shudder: $5.99/mo. or $57.99/yr.

- Sling TV (Sling Orange): $35.00/mo.

- Sling TV (Sling Blue): $35.00/mo.

- Sling TV (Sling Orange + Sling Blue): $50.00/mo.

- Troma Now: $4.99/mo. or $49.99/yr.

- Tubi: Free

- Xumo: Free

- YouTube TV: $64.99/mo.

We don’t have a clue as to what a lot of these services offer, but if you ask them, they’re number one in their category and … growing.

Despite the hysteria surrounding Netflix losing “some” subscribers, corporate entities are keeping their eye on the long game, which is expanding their subscriber base in the largest markets (China, India) and expanding globally to become dominant SVOD and AVOD players.

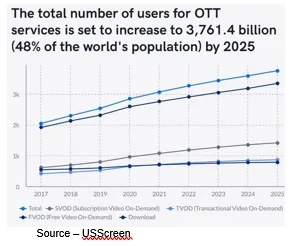

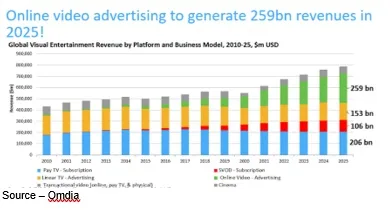

While the economy around the globe is foggy at best, people are intent on taking a break from daily life and escaping for a few hours into the fantasy world of home entertainment.SVOD subscribers are projected to be more than 732M this year, and to grow to more than 1.8B plus by 2027. Revenue is projected to grow from $72.1B to $170.85B.

Initially, the appeal for SVOD was price.

Cut the cable and get a Netflix, Hulu, Amazon Prime account for a fraction of the cost plus the ability to watch it when it was convenient for you, not them! A helluva deal – budget saver, convenience, exclusivity.

As the number of services grew, so did the list of “gotta’ see that” content.

Initially, folks liked the idea of watching everything new they offered all at once and services liked the idea that the more people used their service, the more they’d stick around. But it didn’t happen that way.

Netflix and the other services quickly discovered that there were a lot of people (we’re not in this group) who would plant themselves in front of the screen, consume all the new stuff, cancel the service and move on to the next entertainment buffet.

Yes, there were a lot of advantages to not having to fight to cancel the service as they had done when they left their cable bundle. And what the heck, they could sign up again later when the next batch of new content was released.

Churn – engaging/disengaging the service – became the one measure financial institutions could measure to determine the success or failure of a streaming service throughout the year.

It was much more difficult to focus on the services more important metric – ARPU (average revenue per user – which really determines the streaming service’s long-term profitability, success.

“Consumers were initially faced with an overabundance of high-quality, original content,” Allan McLennan, Chief Executive Officer, PADEM Media Group, noted. “But it didn’t take long for families to start burning through the new content, and then simply add another service because the monthly added cost ($10-$20/mo.) was certainly less expensive than their old cord service. They were starting to learn along the way which was their favorite service and indispensable.

“Until it wasn’t,” he added.

Today, a household might pay $20 a month for Netflix plus $13 for Hulu without ads, then add “a few dollars more” to the entertainment budget to sign up for Disney+ with access to Disney, Pixar and Marvel collections as well as favorite TV shows on Peacock and Paramount+.

And while the family waited for WBD (WarnerBros Discovery) to complete the messy merger of HBO Max and Discovery into one sleek service, they often signed up for both (few consumers pay much attention to the machinations of the M&E industry).

Competition between services became a greater challenge as each worked to set themselves apart from (and above) the other guys.

Streaming was no longer about people cutting cords to get their content direct from the source and cord-cutting was no longer a bargain.

The biggest challenge for today’s services is to capture – and keep – subscribers as all of the organizations are ramping up their production flow to deliver new programming and reconfigure their operations.

McLennan noted that rebundling is already underway.

Disney, which owns Disney+, ESPN+ and controlling interest in Hulu, is encouraging people to bundle the three.

More industry consolidation will deliver more bundling options from the major streamers as organizations balkanize their services.

ViacomCBS has Showtime, BET+, Paramount+, Pluto+ and more to deliver an enticing range of content at an attractive price.

Comcast’s Peacock has NBC, NBC news, CNBC, MSNBC and other services plus a strong reach in Europe through its SkyShowtime service.

WBD (WarnerBros Discovery) is aggressively working to develop a strong, single face to consumers for HBO Max and Discovery as well as their many content services. Despite divergent movie and TV teams/focuses and a $55B debt, the organization is making “progress” with their DTC (direct-to-consumer) service.

The good news/bad news is that all of the services have significant demand for their content libraries which makes it difficult – but not impossible – to unify their services and relationships.

“It will be become difficult for new or smaller players like Lionsgate and AMC Networks to remain stand-alone services and survive,” McLennan said.

“At the same time, services like Disney+, Amazon Prime and Apple TV+ are almost disruption-proof, unless they decide to acquire or develop significant relationships with other services because their parent companies have strong brands and diversified revenue streams,” he noted.

“Contrary to popular rumblings or stock ups and downs,, Netflix won’t fade but will retain its top spot – for the time being – with Disney and HBO Max in second/third position,” McLennan added.

You can expect to see all of the SVODs offering a wide range of creative discounts to tempt subscribers back and encourage them to stay for a number of months, if not for an entire year. You can also expect all of the services to develop and test ad-supported tiers.

Free streaming services, many with advertising, have already grown from 39 per cent of viewers to 47 per cent this year with much lower churn rates as consumers take control of their home entertainment budget and also discover that the AVOD service offers more than just old library content.

AVoD MAU (monthly average user) count is projected to grow from 6.81B to over 8.62B by 2027. AVOD advertising is expected to grow from $50.18B to $91.36B as users shift to the less-expensive services to balance their home entertainment budgets.

This will potentially enable Disney+ Hotstar to lead the AVOD/SVOD streaming leaderboard in three-four years with Netflix maintaining a strong second place followed by HBO Max.

There’s already a tremendous increase in the quality of original scripted dramas/shows and film by all of the major services with increased attention on developing sustained profitability by creative pricing, offers and the consolidation of services.

Content remains the important differentiator for streaming services as we see Netflix, Amazon, Apple, Disney and Paramount develop unique IPs for their portfolios that set them apart from the other services.

The key to retaining a leading position in the streaming service stack will be for organizations to focus more attention on their core activities – an enhanced/natural user interface and a more robust recommendation/selection engine that enables consumers to customize their viewing experience across the paid and free services in their bundle.

When consumers decide to cut the cord to reduce their home entertainment budget, they’ll decide if they need more and will increasingly want/expect that their service(s) actually provide them with even more of the content they want, when they want it.

That’s the way for each of the services to increase their MAU hours … and revenues.

That’s the way for each of the services to increase their MAU hours … and revenues.

As Homelander said in The Boys, “You See: Companies, They Come And Go, But Talent Is Forever.”

He’s right … talent is forever!

# # #

Andy Marken – [email protected] – is an author of more than 700 articles on management, marketing, communications, industry trends in media & entertainment, consumer electronics, software and applications. An internationally recognized marketing/communications consultant with a broad range of technical and industry expertise especially in storage, storage management and film/video production fields; he has an extended range of relationships with business, industry trade press, online media and industry analysts/consultants.