Entertainment is Entertainment, Regardless of the Channel

A few years ago, my wife and I were walking down a street in Zihuantanejo (Mexico) when a VW bug stopped in the middle of the street. A gentleman jumped out of the car and ran over to us, hollering in delight.

It was a waiter from one of our favorite restaurants; and having just arrived, we hadn’t been to see him…yet.

He insisted we come over to the car and meet the family (all six of them), including their 6-month-old.

That evening over dinner, we congratulated him on having another child and commented that the Bug could barely hold everyone.

“Well, the TV broke awhile back and before we could get a new one…,” he responded with a huge grin.

That, my friend, is why the industrial world is facing a declining population!

Worldwide we have:

- 7B people

- 2B households (World Bank)

- 8M connected TVs (Statista)

- 46 percent of world population with internet connection (World Bank)

- 7M Digital TV households (Statista)

- 9B smartphones (Statista)

- N (infinite number) of streaming services

- 24 hrs. in a day

A few things we all agree on are:

- People want to watch stuff – movies, episodic series, how tos, short/long from content. You know stuff!

- Folks like to be entertained on screens – huge screens, big ones, medium-sized, handheld units

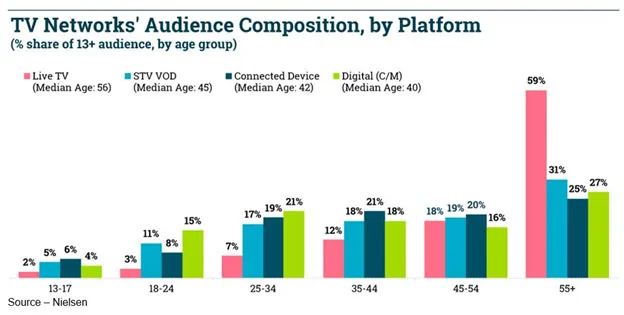

- Different age groups experience their content in different ways and familiarity has become the norm

- Video creators want to create content and be paid for their work/efforts

- People like/prefer free content but in a pinch, most will pay for it

- No one likes ads. (Actually, they don’t like bad ads, 10 of the same ad in hour, ads that they’re not interested in.)

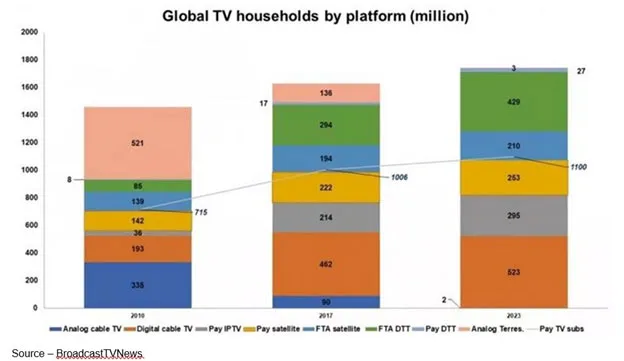

According to Digital TV Research, pay-TV subscribers will surpass 1.1B by 2023 and that many providers are encouraging IPTV conversion because it is more profitable.

Global multichannel surpassed 50 percent last year and should increase to 61.2 percent over the next five years. That resulted in $230-plus billion in service revenues last year and is expected to grow to $245.5B by 2023.

GfK MRI notes that viewers who maintain their TV bundles do it because:

- They’re used to it

- It’s convenient, everything in one place

- Predictable

- See no reason to change, learn new things

For the 90M Americans subscribing to cable packages, TV is still viewed as channels with predictable, assigned numbers that are on at scheduled times with commercial breaks.

However, mobile apps and digital distribution have opened the door for a new type of viewing convenience that the younger crowd took to immediately – VOD.

Globally, about 26 percent of the world is under 15 years of age and some 9 percent is over 64 years of age. Regardless of the country, they all watch their entertainment in different ways.

As a result, and based on fallible logic:

- Kids always have their smartphones with them and on.

- Voice traffic has become almost non-existent on the wireless services, while data consumption has increased to the point it is 70 percent of wireless traffic.

- Folks generally sign up for the convenience of smartphone streaming – anywhere, any time.

- People are obviously using their handheld devices, and this will increase in the near future when 5G becomes “widely, instantly” available (hint – 2025).

- Voice recognition, search is growing rapidly; so regardless of the device, people will be able to “tune to” the specific channel/show they want with just a few words.

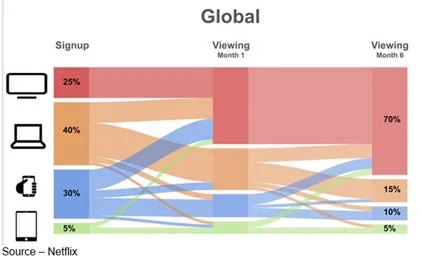

Even Netflix, the leading streaming content service, seems to bear this out because in many of their 190 service countries, people sign up with their smartphone.

And of course, Reid and crew don’t care because they are just interested in increasing their subscribers and staying the big dog in the streaming market.

Netflix will continue to lead in SVoD in both subscriber numbers (outside of China) but will make up only 194 million SVoD customers out of 743 million (26 percent) globally by 2023.

While AT&T rushes to build out it’s 5G E (4G LTE) and 5G services, they are counting on their acquisition of WarnerMedia to deliver 29.6M SVoD homes by 2023 and contribute to the corporate bottom-line with “modest” investment in new content.

Of course, they are far from alone in the new gold rush as free (ad-supported) and subscription, transaction (events) vie to carve out their profitable niche.

Today’s 478M SVoD subscribers will grow to 743M by 2023, with China having the most SVoD subscribers by 2023. However, North America will still drive the largest dollar volume.

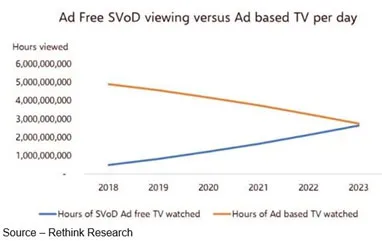

According to Rethink, SVoD is increasing and in terms of hours viewed per day, it will soon draw level with broadcast TV globally by 2023.

Of course, there are “a few” people interested in making their mark here including 6Play, Acorn TV, Alibaba, Altice, Apple, Amazon, América Móvil, AT&T, Awesomeness TV, BritBox, Blim, Baidu, Canal+, CBS, Cinemax, Claro TV, Crackle, dTV, DirecTV, Discovery, Disney, ESPN+, Eurosport, FilmoTV, Fox, France Télévisions, FuboTV, HBO, Hooq, HotStar, Hulu, Iliad’s Free, iQiyi, Kabel Deutschland, KBS, Liberty Global, M6, Magine, Maxdome, MBC, MLB TV, Molotov, MoviStar Play, MTV Play, NBA, NHL, Nickelodeon Play, NTT, Oksusu, Orange Cinema Services, Paramount, PCCW, Philo, PlayStation Vue, Pluto TV, Pooq, PopcornFlix, ProSiebenSat1, Rakuten TV, Reliance Jio, RMC Sport, Roku, RTL, Salto, SBS, SFR-Numericable and oh heck, if we missed you…sorry!

Yes, we did miss a few folks and it was on purpose because they don’t fit into the conventional (old style) service provider or content production/distribution categories … the social media everything to everyone services.

You know:

- YouTube – 1.3B users with 300 hrs. of video uploaded every minute

- Facebook Watch – 2.32B Facebook users

- Alibaba – 636M users

- Tencent – 889 users

- LinkedIn – 437M members

- Twitter – 336M users

- Tumblr, Instagram, Baidu, Sina Wiebo, Vkontakte, Reddits, Taringa, Renren, Zing, Xanga, Mixi, others

Not really competitors?

Wrong!

They seduce eyes away from other content sources so content owners are beginning to search for where eyeballs are at, not where they think they should be … watching them!

Sports venues have already been signing major contracts with them to go where the young viewers are used to looking and the results have been impressive.

The ugly truth is folks don’t think much about the shape or size of the content. Yes, bigger is better but … they’re only there for the content.

Now for the analysts who only see TV as a conventional roster of shows followed by a hodge-podge of dumb, dumber videos, it would appear as though the super competitors (deep pockets) will take over the world and account for all of the incremental growth.

But they overlook the opportunities that fly beneath the radar of the standard fare – docs, mystery, comedy, reality, games, etc. – that were squeezed out of the old TV bundle or never had a snowball’s chance of being considered.

You know religious, quiz, shopping, music, adult, public affairs, government, education and others.

At the same time, there are channels that appeal to expat citizens or residents.

For example, in the US, a strong percentage of citizens are from someplace else (most of us are but that’s a different subject) – Haiti, Mexico, Japan, South Korea, China, India, Australia, Belgium, Russia, Ireland, you name the country/nationality, it’s represented.

People may live and prosper in the US, but no one really wants to forget his/her roots.

Niche channels – both here and abroad – can be very successful and can develop a loyal subscriber base by offering high-quality, distinctive OTT content to viewers direct from their homeland in their native language to keep them in touch, regardless of the distance.

Rethink researchers were more wrong than right when they said SVOD would swamp traditional TV.

VOD across the board will cause its slow demise and we believe advertising will play an important part because done right, people will rush to the content service that offers “free” content.

The difference is that it won’t be the old-fashioned free breaks we escaped from watching the ad – again – to the bathroom or kitchen.

And we can thank technological advances and marketers who weren’t interested in reaching 100M suspects with each ad but really wanted 100,000 interested prospects.

Now that content delivery is to a specific IP address, the content delivery service knows a helluva’ lot about the viewer.

You know, the same data online folks admit to collecting – name, gender, email address, phone number, birthday and location as well as information they collect but don’t brag about – relationship status, line of work, education, race/ethnicity, IP addresses, search history, websites visited, photos/videos/music uploaded, devices used, okay…stuff.

To stop you from screaming and running into a deep, dark cave, let’s say right now that Netflix, Hulu, HBO, Disney, Warner and most of the other SVOD services don’t need (or really want) that much information to develop, deliver content that will keep you subscribing and, in many instances, wasting the weekend to binge something new.

One of the reasons Netflix is so successful is that it curates content, in any language, that would appeal to the nearly 2,000 ‘taste communities’ it identified during its global rollout.

Taste communities are groups of subscribers around the world who are fans of certain types of content, regardless of where they live.

AI (augmented intelligence) and machine learning will enable channels and marketers to personalize the content for the “free content” recipient.

The intelligence and virtually instant customization of ads mean vegetarians don’t get hamburger ads, Jag owners don’t receive a Chevy whatever ad, guys don’t get ads for feminine hygiene products.

Instead, the viewer gets ads with their content that’s tailored to him/her … ads that focus on a specific experience, theme, fan community, interest/preference area.

Sky’s AdSmart platform has already made advances in this area by serving addressable households (those within a defined or targeted audience) different ads during the same TV programming with targeted viewers’ demographics, location, shopping habits and behavioral attributes.

Suddenly, it’s not TV it’s simply your entertainment, news and the information you want–when you want it, on the screen you want it on.

Yep, you’ll be able to finally follow Woody Guthrie’s advice, “Take those ideas, and, uh… and find yourself some place where, uh… where nobody, uh… nobody will bother you, and just put those things down…”

Yep, you’ll be able to finally follow Woody Guthrie’s advice, “Take those ideas, and, uh… and find yourself some place where, uh… where nobody, uh… nobody will bother you, and just put those things down…”

Just don’t think too hard on how you got to glory.

# # #